As an Amazon Associate, I earn a small commission from qualifying purchases. Learn more about this.

When you’re standing at the Alamo rental counter after a long flight, the last thing you want to do is make another complex decision. Extended Protection offers a safety net, but is it necessary?

Balancing safety and budget is a tricky endeavor, and this post aims to help you strike the right balance.

Alamo Extended Protection Review

When you’re at the rental counter, or even before that when you’re perusing Alamo’s website, you’ll come across the option to add Extended Protection to your car rental.

Basically, the Extended Protection is an expanded form of insurance that goes beyond the basic liability coverage mandated by most U.S. states.

So, what does it actually cover?

| Features | Alamo Extended Protection | Personal Auto Insurance | Credit Card Benefits |

|---|---|---|---|

| Liability Coverage | ✓ | ✓ (Check your policy) | ✗ |

| Uninsured Motorist Coverage | ✓ | ✓ (Check your policy) | ✗ |

| Comprehensive and Collision | ✗ | ✓ (Check your policy) | ✓ (Typically) |

| Medical Expenses | ✗ | ✓ (Check your policy) | ✗ |

| Personal Property Coverage | ✗ | ✓ (Check your policy) | ✗ |

| Towing | ✗ | ✓ (Check your policy) | ✓ (Typically) |

| Coverage Outside the U.S. | Varies | Rarely | Varies |

| Daily Cost | $ (Varies) | Included in personal policy | Included with card use |

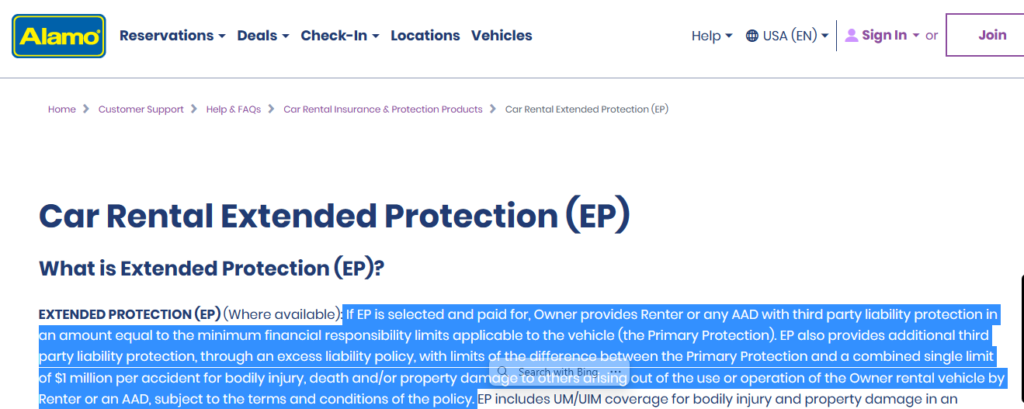

Alamo’s Extended Protection generally covers two main areas: additional liability insurance (ALI) and uninsured or underinsured motorist coverage (UM/UIM).

The additional liability insurance extends the amount that will be paid out for third-party bodily injury or property damage claims. This is particularly important if you find yourself in an unfortunate situation where you are at fault in an accident.

Your liability toward others’ medical bills or property damages could easily run into thousands of dollars; having the ALI can help protect your finances in such scenarios.

Then there’s the UM/UIM coverage, which is designed to protect you if you’re in an accident and the other driver is at fault but doesn’t have sufficient insurance to cover your expenses.

This can be a lifesaver in many cases, especially if medical bills are involved. While the details can vary based on your location and specific rental agreement, the general idea is to provide a layer of financial security that goes above and beyond the basic coverage.

Now, here’s where it can get tricky: Alamo’s Extended Protection isn’t your only option for these types of coverage.

Your personal auto insurance might already offer similar protections, so it’s crucial to know your existing policy inside and out before opting in or out of Alamo’s offer.

Additionally, some credit card companies offer complimentary rental car insurance if you book the rental using their card. However, credit card insurance often only offers collision damage waiver (CDW), not liability insurance, so you’ll need to weigh your options carefully.

The cost of Alamo’s Extended Protection varies depending on various factors such as location, type of car, and duration of the rental.

It’s usually priced per day, adding an extra fee on top of your base rental rate.

While this might seem like just another expense to tack onto your travel budget, for some people, the peace of mind it offers can be worth every penny.

Is Alamo Extended protection worth it?

The short answer is, it depends.

I know, not the most satisfying response, but hear me out.

The worthiness of Alamo’s Extended Protection can be subjective and varies depending on individual circumstances, travel plans, and existing insurance coverage.

Let’s break it down into a few key considerations:

Your Existing Insurance Coverage

The first thing you should do is take a good look at your own auto insurance policy. Many people already have substantial liability coverage, as well as underinsured or uninsured motorist coverage, through their personal auto insurance.

If your policy provides high limits and broad coverage, the additional coverage from Alamo might be redundant. However, it’s crucial to confirm whether your existing policy covers rental cars; some don’t.

International Travel

If you’re renting a car outside your home country, your domestic insurance may not cover you, making the Extended Protection a smart move.

Similarly, certain states or countries have specific insurance requirements that your regular policy might not meet. Do your research and know the rules of the road in the area you’ll be visiting.

Your Financial Comfort Zone

The idea behind insurance is to mitigate financial risk. If you can easily cover the costs associated with a potential accident—be it medical expenses, car repairs, or legal fees—then you might opt to skip the additional coverage.

However, if the thought of such expenses gives you heart palpitations, the daily cost for Extended Protection could offer invaluable peace of mind.

Duration and Nature of Your Trip

If you’re planning a long road trip through unfamiliar or high-traffic areas, the chances of an accident, however minor, could be higher.

In these cases, paying for extended protection might be a wise decision. Conversely, if you’re just renting a car for a day or two and won’t be driving much, you may decide the additional cost isn’t justified.

Final Thoughts

Understanding how Alamo’s Extended Protection works is key to deciding whether it’s the right choice for you. Do your homework, know what your existing insurance covers, and make sure to read all the fine print before making your decision.